W-2 Wage Calculation Revenue Procedure for §199A Released in Final Form by IRS

The final regulations under §199A state that the IRS may provide for methods of computing taxable wages.[1] At the same time as the final regulations were issued, the IRS finalized a revenue procedure to provide for acceptable methods of computing W-2 wages.

Revenue Procedure 2019-11 provides for methods of computing W-2 wages for purposes of IRC §199A. The revenue procedure was issued during 2018 in draft form, and the final version has no significant changes from the original proposed version.

The Revenue Procedure begins the Rules of Application in Section 3 with the following caution on wages that can and cannot be included in the calculation of §199A W-2 wages:

In calculating W-2 wages for a taxable year under the methods described in this revenue procedure, include only wages properly reported on Forms W-2 that meet the applicable rules of § 1.199A-2(b). Specifically, § 1.199A-2(b)(2)(i) provides that, except as provided in § 1.199A-2(b)(2)(iv)(C)(2) (concerning short taxable years that do not include December 31) and § 1.199A-2(b)(2)(iv)(D) (concerning remuneration for services performed in the Commonwealth of Puerto Rico), the Forms W-2, “Wage and Tax Statement,” or any subsequent form or document used in determining the amount of W-2 wages are those that are issued for the calendar year ending during the person’s taxable year for wages paid to employees (or former employees) of the person for employment by the person. Section 1.199A-2(b)(2)(i) also provides that, for purposes of § 1.199A-2, employees of the person are limited to employees of the person as defined in section 3121(d)(1) and (2) (that is, officers of a corporation and employees of the person under the common law rules). Therefore, Forms W-2 provided to statutory employees described in section 3121(d)(3) (that is, Forms W-2 in which the “Statutory Employee” box in Box 13 is checked) should not be included in calculating W-2 wages under any of the methods described in this revenue procedure.

The Revenue Procedure at Section 3.02 warns that this Revenue Procedure’s determination of wages is solely for §199A purposes, and the procedure has no application in determining wages for other purposes such as for FICA taxation, FUTA taxation or payments subject to federal income tax withholding.

After reciting the W-2 wages definition from the proposed regulations, in Section 4.02 the IRS provides a mapping of W-2 information to what is and is wages for IRC §199A purposes.

.02 Correlation with Form W-2. Under the 2018 Forms W-2, the elective deferrals under section 402(g)(3) and the amounts deferred under section 457 directly correlate to coded items reported in Box 12 on Form W-2. Box 12, Code D is for elective deferrals to a section 401(k) cash or deferred arrangement plan (including a SIMPLE 401(k) arrangement); Box 12, Code E is for elective deferrals under a section 403(b) salary reduction agreement; Box 12, Code F is for elective deferrals under a section 408(k)(6) salary reduction Simplified Employee Pension (SEP); Box 12, Code G is for elective deferrals and employer contributions (including nonelective deferrals) to any governmental or nongovernmental section 457(b) deferred compensation plan; Box 12, Code S is for employee salary reduction contributions under a section 408(p) SIMPLE (simple retirement account); Box 12, Code AA is for designated Roth contributions (as defined in section 402A) under a section 401(k) plan; and Box 12, Code BB is for designated Roth contributions (as defined in section 402A) under a section 403(b) salary reduction agreement. However, designated Roth contributions are also reported in Box 1, Wages, tips, other compensation and are subject to income tax withholding.

The proposed Revenue Procedure provides three methods that can be used to compute W-2 wages for §199A purposes. They are:

Unmodified Box Method;

Modified Box 1 Method; and

Tracking Wages Method.[2]

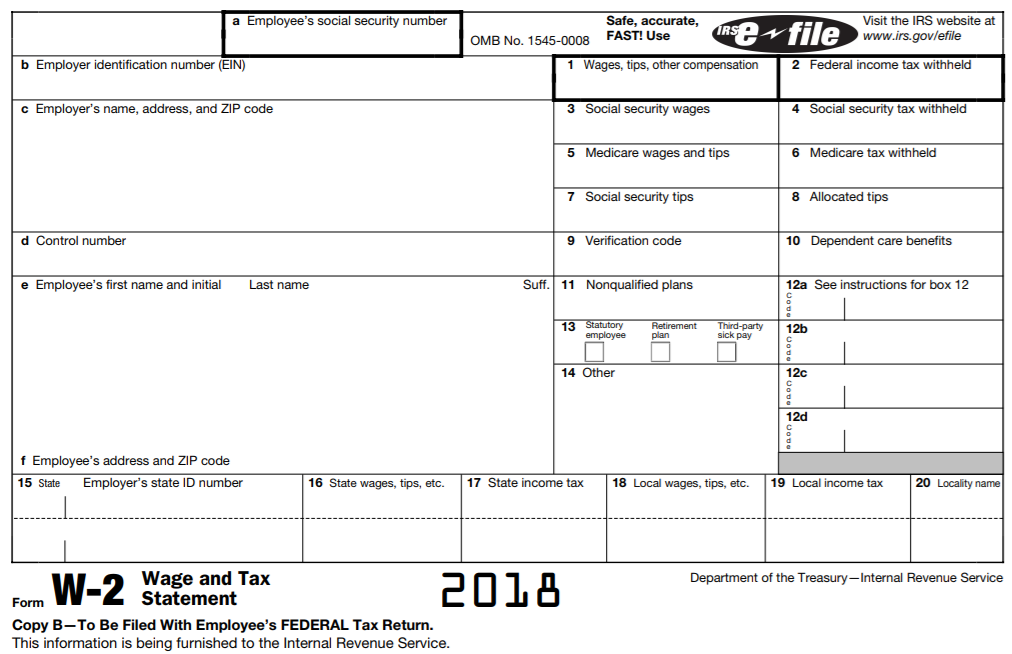

The methods are described below. For reference, here is a copy of 2018 Form W-2 that will be referred to in the proposed Revenue Procedure.

2018 Form W-2

Unmodified Box Method

The proposed Revenue Procedure defines the unmodified box method as follows:

Under the unmodified box method, W-2 wages are calculated by taking, without modification, the lesser of—

(A) The total entries in Box 1 of all Forms W-2 filed with SSA by the taxpayer with respect to employees of the taxpayer for employment by the taxpayer; or

(B) The total entries in Box 5 of all Forms W-2 filed with SSA by the taxpayer with respect to employees of the taxpayer for employment by the taxpayer.[3]

Box 1 is the box holding taxable wages, tips and compensation. Box 5 represents the Medicare wages and tips.

Modified Box 1 Method

The second method described in the proposed Revenue Procedure is the modified box 1 method.

Under the Modified Box 1 method, the taxpayer makes modifications to the total entries in Box 1 of Forms W-2 filed with respect to employees of the taxpayer. W-2 wages under this method are calculated as follows—

(A) Total the amounts in Box 1 of all Forms W-2 filed with SSA by the taxpayer with respect to employees of the taxpayer for employment by the taxpayer;

(B) Subtract from the total in paragraph .02(A) of this section amounts included in Box 1 of Forms W-2 that are not wages for Federal income tax withholding purposes, including amounts that are treated as wages for purposes of income tax withholding under section 3402(o) (for example, supplemental unemployment compensation benefits within the meaning of Rev. Rul. 90-72); and

(C) Add to the amount obtained after paragraph .02(B) of this section the total of the amounts that are reported in Box 12 of Forms W-2 with respect to employees of the taxpayer for employment by the taxpayer and that are properly coded D, E, F, G, and S.[4]

Tracking Wages Method

The final method taxpayers would be able to choose from under the proposed Revenue Procedure is the tracking wages method. The procedure describes that method as follows:

Under the tracking wages method, the taxpayer actually tracks total wages subject to federal income tax withholding and makes appropriate modifications. W-2 wages under this method are calculated as follows—

(A) Total the amounts of wages subject to federal income tax withholding that are paid to employees of the taxpayer for employment by the taxpayer and that are reported on Forms W-2 filed with SSA by the taxpayer for the calendar year; plus

(B) The total of the amounts that are reported in Box 12 of Forms W-2 with respect to employees of the taxpayer for employment by the taxpayer and that are properly coded D, E, F, G, and S.[5]

Short Tax Years

The Revenue Procedure describes special rules for a short tax year. In Section 6.01 the proposed Revenue Procedure begins:

.01 Special rule for taxpayers with a short taxable year. In the case of a taxpayer with a short taxable year, subject to the rules of application described in section 3 of this revenue procedure, the W-2 wages of the taxpayer for the short taxable year shall include only those wages paid during the short taxable year to employees of the taxpayer, only those elective deferrals (within the meaning of section 402(g)(3)) made during the short taxable year by employees of the taxpayer, and only compensation actually deferred under section 457 during the short taxable year with respect to employees of the taxpayer. See § 1.199A-2(b)(2)(iv)(C) of the regulations.

A taxpayer is required to use the tracking wages method for a short taxable year. The method is applied in the following manner:

.02 Method required for a short taxable year and modifications required in application of method. The W-2 wages of a taxpayer with a short taxable year shall be determined under the tracking wages method described in section 5.03 of this revenue procedure. In applying the tracking wages method in the case of a short taxable year, the taxpayer must apply the method as follows—

(A) For purposes of section 5.03(A), the total amount of wages subject to federal income tax withholding and reported on Form W-2 must include only those wages subject to federal income tax withholding that are actually or constructively paid to employees during the short taxable year and reported on Form W-2 for the calendar year ending with or within that short taxable year (or, for a short taxable year that does not contain a calendar year ending with or within such short taxable year, wages subject to federal income tax withholding that are actually or constructively paid to employees during the short taxable year and reported on Form W-2 for the calendar year containing such short taxable year); and

(B) For purposes of section 5.03(B), only the portion of the total amounts reported in Box 12, Codes D, E, F, G, and S on Forms W-2, that are actually deferred or contributed during the short taxable year are included in W-2 wages.

Additional Computations May Be Needed

The Revenue Procedure warns in Section 2 that adjustments may need to be made to any of these figures to obtain the W-2 wages properly allocable to a particular trade or business:

W-2 wages calculated under this revenue procedure are not necessarily the W-2 wages that are properly allocable to QBI and eligible for use in computing the section 199A limitations. As mentioned above, only W-2 wages that are properly allocable to QBI may be taken into account in computing the section 199A(b)(2) W-2 wage limitations. Thus, after computing W-2 wages under this revenue procedure, under § 1.199A-2(b)(3), the taxpayer must determine the extent to which the W-2 wages are properly allocable to QBI. Then, the properly allocable W-2 wages amount is used in determining the W-2 wages limitation under section 199A(b)(2) for that trade or business as well as any reduction for income received from cooperatives under section 199A(b)(7).